WS EkinsGuinness Dynamic Growth Fund

Overview

Summary

- Dynamic asset allocation between equities, bonds, commodities and cash

- Aim is to capture equity market upside in bull markets but to reduce drawdowns (peak to trough falls) in bear markets

- All exposure achieved through Exchange Traded Funds which have low costs and low dealing charges

- Avoids style bias – both asset allocation and equity focus change according to market conditions

- Suitable as a core holding for investors who prefer not to make asset allocation changes themselves

- Also acts as a potential diversifier within a broader portfolio due to generally low correlation and lower volatility than Equities

Investment Approach

The two most important drivers for investment decisions are fundamental value and market trends. Fundamental value determines the potential over the medium/long term but can be a poor indicator of price movements in the short term. Market trends (including momentum and overbought signals) can be a good leading indicator of future price movements but can be dangerous if fundamental value is ignored. Neither analytic should be used in isolation but it is logical to select investments based objectively according to a combination of fundamental value and market trends which are independent of opinion, forecasts and emotion.

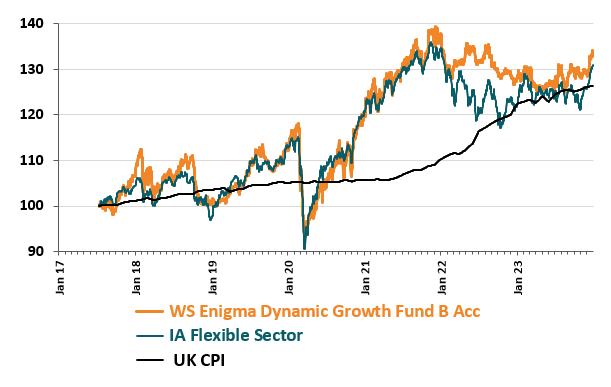

Performance

| Dec 23 | 1 Yr | 3 Yrs | 5 Yrs | Launch* | |

|---|---|---|---|---|---|

|

Fund |

3.4% |

4.5% |

11.6% |

33.6% |

34.1% |

|

IA Flexible |

4.0% | 7.1% | 8.5% | 33.9% | 30.4% |

|---|

|

IA Flexible |

4.0% | 7.1% | 8.5% | 33.9% | 30.4% |

|---|

|

IA Flexible |

4.0% | 7.1% | 8.5% | 33.9% | 30.4% |

|---|

Performance shown is the total return (net of fees & costs) for the Accumulation B share class. Inception date was 12 July 2017. The Fund is not managed against any benchmark. The Investment Association Flexible Sector and UK Consumer Price Inflation are shown as Comparator benchmarks as per FCA PS 19-04. The IA Flexible Sector contains a wide array of funds with a flexible mandate, hence the comparator, but many of them have different investment objectives and profiles. Past performance is not a reliable indicator of future performance. Source: Ekins Guinness LLP.

Key Facts

Structure & Adminsitration

| Structure |

UCITS / ISA |

Authorised Corporate Director |

Depositary | Custodian | Auditor |

Income / Accumulation |

Dividend Payment Dates |

Valuation & Cut Off |

Comparator Benchmark |

|---|---|---|---|---|---|---|---|---|---|

|

UK Authorised OEIC |

Yes |

Waystone Financial Services |

NatWest |

Northern Trust |

Copper Parry |

Both |

31 January & 31 July |

12 noon daily |

MSCI World Index |

Share Classes

| Share Class | Minimum |

ACD Fixed Fee |

Ongoing Charges Figure |

ISIN | SEDOL |

|---|---|---|---|---|---|

|

Z Accumulation GBP |

£200,000 |

0.45% |

0.70% |

GB00BQ1L7137 |

BQ1L713 |

|

Z Income GBP |

£200,000 |

0.45% |

0.70% |

GB00BQ1L7244 |

BQ1L724 |

|

B Accumulation GBP |

£5,000 |

0.70% |

0.95% |

GB00BLFFG644 |

BLFFG64 |

|

B Income GBP |

£5,000 |

0.70% |

0.95% |

GB00BLFFGB97 |

BLFFGB9 |

Managers

Charles Ekins

Charles is the founder and Chief Executive of Ekins Guinness LLP. Previously he was Chief Investment Officer at Valu-Trac Investment Management, prior to which he spent 19 years at Morgan Grenfell (Deutsche) Asset Management where he was a portfolio manager, member of the Investment Policy Committee and client director. He read Maths with Computing Science at Bristol University and has an MBA from the City University Business School. Charles is a Director of the Herald Worldwide Technology Fund (Dublin OEIC).

Jasper Falk

Jasper has over 20 years experience in Investment Banking. He established and managed JPMorgan’s Global Inflation trading business which assisted Pension Funds and Asset Manager clients in hedging and managing their liabilities. He was also a member of the Fixed Income Management Committee. Jasper read Engineering and Management Studies at St Catharine’s College Cambridge, and holds the Financial Times Non-Executive Director Diploma.

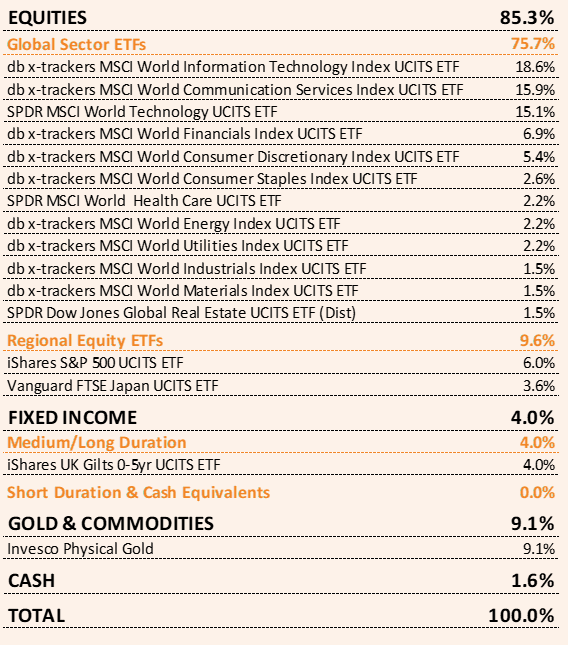

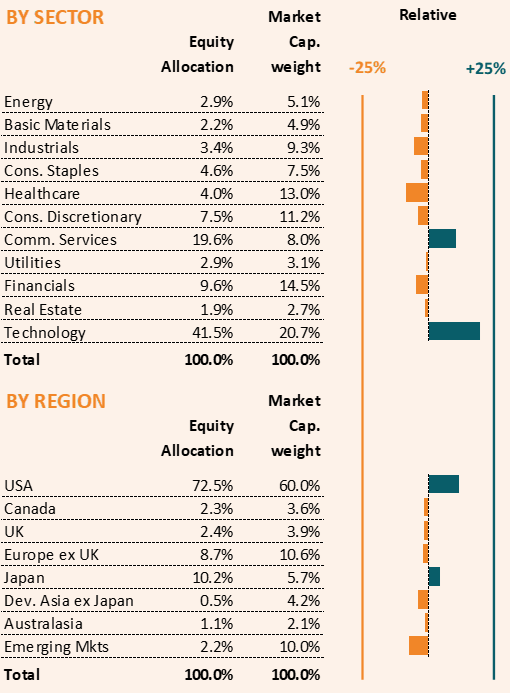

Holdings

Portfolio Holdings

Equity Analysis

Investment Commentary

as at 31 December 2023

as at 31 December 2023

The Fund returned 1.1% in November 2023. This gives a return for the year-to-date of 1.3% and a return since launch (7 July 2017) of 29.6% (net of fees and costs).

Since launch, the Fund is in the second quartile of the Investment Association Flexible Sector, and is ahead of all four Investment Association Mixed Asset Sectors (Flexible, Mixed Investment 0-35%, 20-60% & 40-85% Shares). It is also in the top quartile of the combined four IA Mixed Asset Sectors over 3 and 5 years (consisting of 627 funds).

Equities had a very strong run in November, returning 8.3% in local price terms which, due to the weak US Dollar, equates to 4.8% in GBP terms. It was driven by the continued fall in US inflation such that investors are enthused that the much-anticipated end to rate tightening is now a realistic prospect and that interest rates will be cut, possibly significantly, in 2024.

Bond markets also performed well in November, but this was after a very weak period beforehand and a previous spike in yields. Both US Treasuries and UK Gilts have delivered negative

returns so far in 2023. Gold was up 2.7% in November and is up 12% this year, but Oil fell 5% and is down 4% for the year.

At the Sector level, Technology was the strongest performer in November (+8.9% in GBP terms), whereas Energy was down 3.8% due to the weak Oil price. This highlights the disparity of returns between Sectors, which has been a feature of markets all year. The return from Technology year-to-date of 40% contrasts with Utilities which has returned -7%. Staples, Healthcare, Energy & Real Estate) have all given a negative return this year.

The main change in the Fund during the month was a significant increase in the Equity allocation. Prior to the strong November rally, world equities had been in a downtrend and there had been concerns that a repeat of the 2022 bear market was possible. Equities in the US, Europe ad UK remain vulnerable to economic slowdown (due to low money supply and delayed reaction to higher interest rates) but economic growth elsewhere (especially Asia) means that a global recession is unlikely. The bull argument for Equities is essentially that there is plenty of scope to cut interest rates.

Our model had previously had a fairly low allocation to Equities because of a warning signal in August which resulted in a meaningful fall in Equities and a new downtrend.

For much of the time, a change in market direction does not have an immediate or significant impact on our asset allocation model – the model seeks to capture medium/long term trends rather than focusing on short term trends (unless valuation is extreme and/or there are other short term risk flags).

However, the November rally did cause an almost immediate increase in Equity allocations. The reason is that the strength of the rally triggered a shift from medium/long term Price trends that had been falling to rising. Unless there is now a sharp fall in Equities, the Price index is sufficiently above the Trend levels that the Trend lines are likely to keep rising.

We are not under any illusions that the outlook for Equities could deteriorate again, just like in August. However, the expectation that interest rates have peaked and will fall in 2024 is a powerful stimulant for Equity markets. Furthermore, the US Federal Reserve is injecting liquidity in the financial system again, which is also positive for markets. The surprise in 2023 has been the resilience of the US economy despite very weak money supply numbers – it may just be a case of a delayed impact and the money supply numbers might still cause a recession. Over the next six months there is still a risk of pressure on corporate earnings which could negatively impact Equities.

Sometimes it is the case that our Asset Allocation has significant changes over a fairly short time period. When this happens, it is often a reflection of general market uncertainty and rapid changes in sentiment. More often than not, markets settle back down into a medium/long term trend, and this is when the greatest opportunities occur. It is important to be on the right side of these longer term trends when they occur, so we think it is worth repositioning the allocations as these trends change, even if the allocations are are a bit more variable than normal.

Documents

Specific to WS Enigma Dynamic Growth Fund

Specific to Fund Umbrella

Links to external sites

Umbrella Documents

Reports

How to Invest

via Platforms

Directly

The WS Enigma Dynamic Growth Fund is available on the following platforms:

Contact Ekins Guinness LLP

Contact Waystone Fund Services

| Allfunds | Aegon | AJ Bell | Alliance Trust |

|---|---|---|---|

|

Ascentric |

Aviva |

Barclays |

FNZ |

|

Hargreaves Lansdown |

Interactive Investor |

Novia |

Nucleus |

|

Pershing |

Transact |

Zurich |

|

- Call 01264 738989

- Link to Application Forms

- Call 01264 738989

- Link to Application Forms